Why Real-Time Policy Monitoring Is the Single Most Important Feature When Choosing COI Tracking Software

Real-time policy monitoring is the single most important feature in COI tracking software because a certificate of insurance is proof of coverage only on the day it was issued, and insurance policies change roughly five times per year on average, per Certificial's 2026 product data. Static certificate tracking cannot detect mid-term cancellations, limit reductions, or schedule modifications, which is where uninsured claims occur. Smart COI technology connects directly to the insurance agent's management system and reflects any policy change within seconds. Without that connection, COI tracking software is document management rather than risk management. Last updated: May 2026

Most companies choose certificate of insurance (COI) tracking software to "automate certificate collection." Six months later, they have the same compliance headaches, just digitized. The fundamental question buyers never ask: "Can this software tell me if my vendor's coverage is actually valid right now?"

That single question separates document management from risk management.

Three Scenarios Where Certificate Tracking Fails

Scenario 1: Mid-Term Cancellation

January 15: Vendor submits a compliant COI for their delivery fleet.

March 20: Carrier cancels Auto Liability policy for non-payment.

April 5: Vendor's driver causes $250,000 accident on your property.

What traditional COI tracking shows: Green checkmark, certificate on file through December 31.

Actual coverage status: Zero. Policy cancelled 16 days before the accident.

Christopher A. Arcitio, Of Counsel at Kaufman Dolowich LLP, explains what happens legally: "If a subcontractor's insurer validly cancels a subcontractor's policy, General Contractors can find themselves litigating personal injury lawsuits on their own, without the benefit of a subcontractor's insurance policy at play... insurance companies must mail a timely notice of cancellation to the insured and the insured's authorized agent or broker. However, they generally do not need to inform anyone else in order to cancel the policy - which includes a certificate holder."

The court's position is equally stark: "New York courts may argue that the general contractor cannot rely upon the COI since 'the policy was not in existence at the time of the accident' and, as such, there was no coverage under an insurance policy."

Your exposure: Full $250,000 claim falls to your insurance, plus potential premium increases of 20-30%.

Scenario 2: The Schedule Modification

January 15: Vendor submits a compliant COI for their delivery fleet.

February 20: Subcontractor purchases a new truck but fails to add it to the Auto Liability policy schedule.

March 15: An accident involving the new truck occurs on your job site.

What traditional COI tracking shows: Valid Auto Liability policy on file.

Actual coverage: The truck's VIN is not insured under this Auto Liability schedule.

Christopher A. Arcitio, Of Counsel at Kaufman Dolowich LLP, explains what happens legally:

"if a policy limits coverage to listed automobiles and an unlisted vehicle causes an accident with bodily injuries, the contractor's options become severely limited. In personal injury litigation, plaintiffs typically pursue defendants with insurance coverage, not uninsured defendants. Even when construction contracts require subcontractors to maintain current liability insurance and name the contractor as additional insured, a carrier's coverage disclaimer leaves the contractor exposed. The contractor cannot transfer the lawsuit to the subcontractor's insurer, forcing the contractor's own carrier to defend through trial."

Cost: Another uninsured claim your insurance must defend, with no ability to transfer to the subcontractor's carrier.

Legal Precedent: WAINWRIGHT v. et al., Third-Party Defendants

This NY court case shows what happens when a Subcontractor's (or Supplier)'s insurance is canceled unbeknownst to the Certificate Holder's risk team.

A General Contractor secured a compliant COI from their sub. The policy was then canceled mid-term for nonpayment, and later an accident happened. Their insurer had no obligation to provide coverage, leaving the General Contractor - who relied on the outdated COI - holding the bag. Here's the link to the actual court ruling.

Why Notice of Cancellation Endorsements Fail

Many companies require Notice of Cancellation endorsements as a solution. Matthew Dobras from PowerFlex explains why this doesn't work at scale: "Collecting endorsements for Notice of Cancellation is notoriously difficult, especially when you're working with a large network of subcontractors and vendors. Even when you do get them, they're often ineffective: they can be delayed, misplaced, or buried in a mailroom."

Legally, these endorsements provide no protection. Arcitio notes that courts have rejected claims that certificate holders should be notified: "At least one New York court rejected an argument that a general contract should have been notified of a cancellation as an additional insured even after the subcontractor had a 'courtesy' policy of notifying additional insureds of a cancellation. The court argued that the COI also stated that the insurer had no obligation or liability of any kind for the insurance company's alleged failure to mail a 30 days written notice."

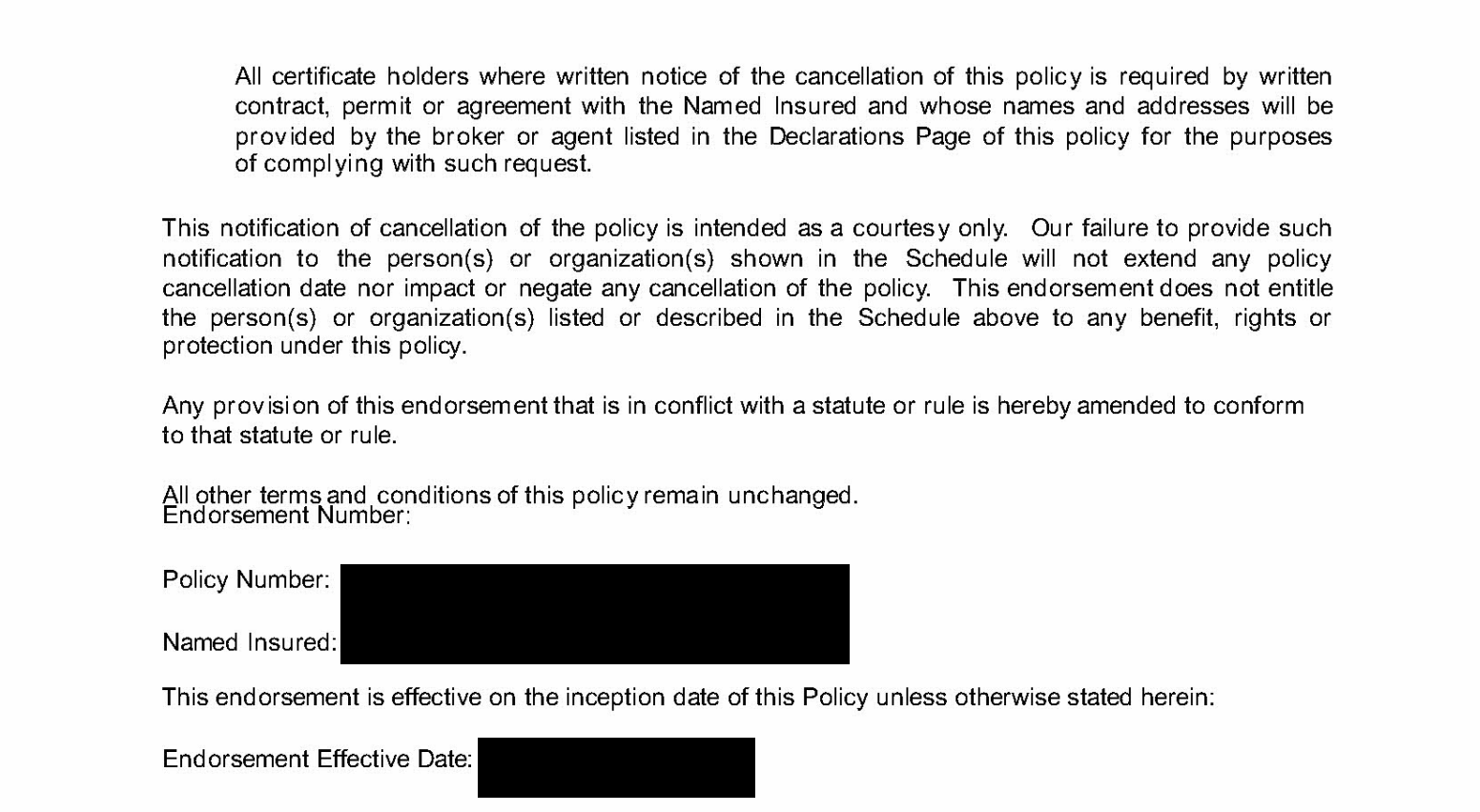

Here'a one example of an endorsement that specifically states: "This notification of cancellation of the policy is intended as a courtesy only. Our failure to provide such notification to the person(s) or organization(s) shown in the Schedule will not extend any policy cancellation date nor impact or negate any cancellation of the policy. This endorsement does not entitle the person(s) or organization(s) listed or described in the Schedule above to any benefit, rights or protection under this policy."

The only effective alternative: "Systems that detect insurance policy cancellations immediately as they occur, without relying on timely 30 Days notices would ensure GCs have viable subcontractors with legitimate insurance for risk transfer when personal injury accidents happen."

Smart COIs: The Only Real-Time Policy Monitoring Technology

Traditional COI tracking operates on static PDFs:

Data source: vendor-submitted document

Update mechanism: manual re-collection

Change detection: only at scheduled intervals

It can confirm a certificate exists in your files and verify it met requirements when submitted. It cannot detect mid-term cancellations, coverage reductions, or schedule-level changes.

Real-time policy monitoring via Smart COI technology solves the faulty approach: it connects directly to insurance agent management systems.

Data source: live policy database

Update mechanism: automatic sync every 15 minutes

Change detection: within seconds of the Agent making changes

It provides policy status (active, cancelled, expired), immediate notification of changes, schedule-level monitoring of specific vehicles and equipment, and automatic updates when policies renew.

Think of it like managing finances. Quarterly bank statements tell you what your balance was on a specific day. Your banking app shows your current balance updated in real-time. Traditional COI tracking is the quarterly statement. Real-time policy monitoring is the app on your phone.

ROI on Risk Mitigation via Smart COIs

"Automated COI tracking systems that update certificates in real-time provide substantial benefits. They reduce administrative burdens on insurance agents and brokers who spend significant time manually listing covered assets on certificates. By ensuring COIs update simultaneously with policy changes, these systems reduce agents' exposure to errors and omissions claims while giving contractors the current documentation they need for legal protection." - Christopher A. Arcitio, Of Counsel at Kaufman Dolowich LLP.

Average claim costs:

- General Liability $30,000-$75,000

- Workers' Compensation ~$40,000.

- Auto Liability $50,000-$100,000

- Property Damage $100,000+

- Construction defects: hundreds of thousands.

Cascade costs beyond the claim: project delays when work stops, premium increases of 20-30% after uninsured incidents, litigation expenses even when not liable, reputation damage affecting client relationships.

Features Smart COI Technology Makes Obsolete

Real-time policy monitoring eliminates the need for traditional COI tracking features:

Vendor submission portals: Agents submit directly through integrated systems; vendors never touch certificates, eliminating fraud vulnerability entirely.

Email reminder automation: Policies update automatically at renewal; no vendor action required, no renewal season email campaigns needed.

Expiration date tracking systems: Real-time monitoring shows policy status regardless of certificate expiration date; mid-term cancellations detected immediately, not just expirations.

Certificate review workflows: Automated compliance verification with live policy data replaces staff review of each certificate - or OCR/AI offered by some COI tracking tools.

Document re-collection processes: Certificates update automatically when policies change; no requesting updated documents when changes occur.

Cancellation notice endorsement tracking: Real-time policy monitoring provides instant cancellation notification, replacing reliance on 30-day carrier notices that often never arrive.

Seven Critical Evaluation Questions

- Does your platform monitor insurance policies in real-time, or track certificate documents?

- How quickly does your system detect a mid-term policy cancellation?

- Can vendors submit certificates directly to your platform?

- Does your platform track schedule-level details like specific vehicle VINs or equipment serial numbers?

- What compliance rates do your current customers achieve?

- How does renewal work in your system?

- How do you verify certificates are legitimate and not fraudulent?

The Core Choice

If you’re tasked with finding an insurance compliance solution for your company, you're not choosing between COI tracking platforms with slightly different features. You're choosing between software that manages static certificate documents more efficiently and Smart COI technology that monitors actual insurance coverage continuously. The key COI tracking features that don’t include Smart COI technology have serious limitations:

Compliance automation without real-time monitoring helps with efficient document filing.

OCR extraction without policy connection means faster data entry for outdated information.

Email renewal reminders without automatic updates result in organized renewal chase.

Dashboards without live data equal better visualization of stale information.

Real-time policy monitoring equals actual risk management.

When evaluating COI tracking software, start with questions that actually matter:

- Does this platform monitor insurance policies in real-time, or does it just manage certificate PDFs?

- Does this tool have Smart COI technology?

- If a Supplier (Sub) cancels a policy mid-term, will I know immediately?

- If a Supplier (Sub) adds/removes assets to/from schedule, will I know immediately?

- If I already obtained a COI once, will I receive an updated copy automatically when it’s time to renew, or would I need to chase the Supplier for an updated copy?

C.svg)